WEEKLY MARKET BRIEF │ JANUARY 14, 2025

Optimism abounds, or so it appears.

The second week of January demonstrated signs of pent up market activity releasing, as if the dam might be breaking. OK, not quite that dramatic.

The first two weeks of showing activity are the busiest on record, just edging out 2021 and 2022, ending last week with just over 21,000 showings across the Denver MSA. The same week last year had just 12,300 showings.

But buyers are still demonstrating patience as last week it took just over 36 showings for the average property to go under contract and contract volume (592) was slightly under 2024 (641). While lots of buyers are out looking, they are simply in no rush.

Conservely, seller activity was strong with 989 new properties listed for sale, the third highest-second week of the year over the last 12 years.

Inventory is climbing, days on market coming down, concessions are holding steady and prices are up (sort of).

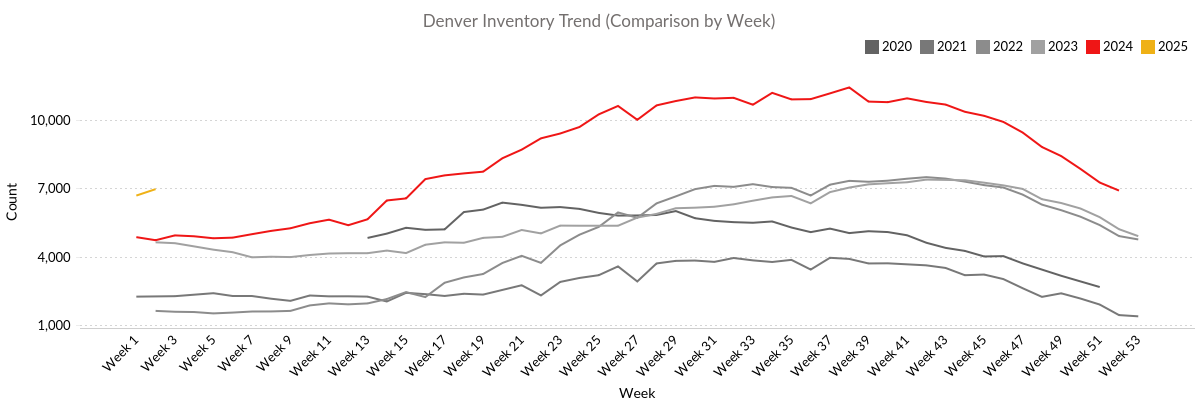

Inventory

Homes for sale hit 6,957 last week with 989 new listings hitting the market, greatly reduced withdrawn and expired properties and only a modest number of new contracts. Last year the Denver MSA hit 11,412 homes as the highest point of inventory, yet we started out the year with only 4,700 homes on the market.

While there are many variables (with interest rates being the most significant) that will influence what inventory levels we hit in 2025, with a pent up desire by sellers to move after almost 3 years of a slower market I wouldn’t be surprised to see inventory touch 15,000 homes.

If we do hit this level of inventory, home values will only modestly appreciate. But make no mistake, if rates drop below 6%, we’ll see buyers making faster decisions, more market volume, suppressed inventory and a strong appreciation market.

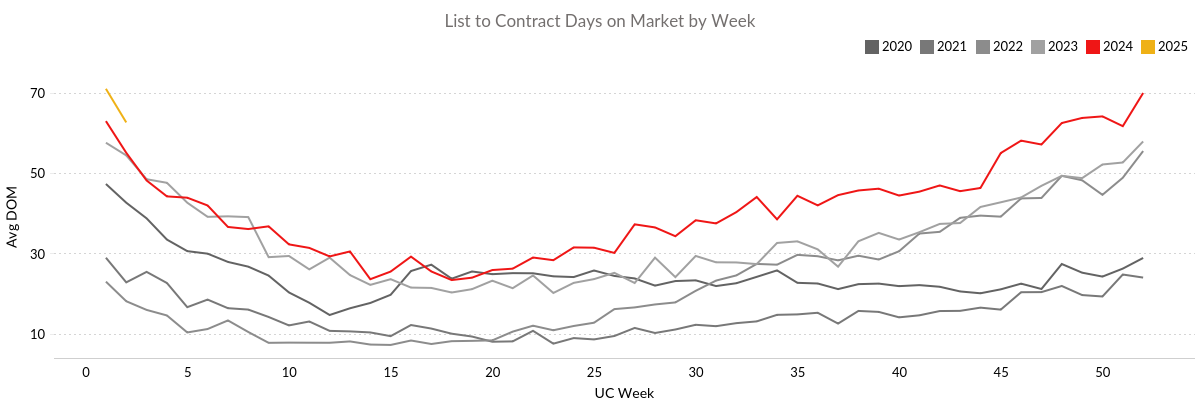

Days on Market

The end of each year is painful for sellers as days on market climbs, showings reduce and price reductions are the norm. But the beginning of each year brings new hope and already the thorn in most sellers’ side (how long will my home be on the market) is showing signs of the seasonal shift we expect.

Days on market hit a 12 year high in December and week one of January this year pushed that record even higher, touching 71 days on average. But already week two of the year is bringing sellers some hope, showing a drop in days on market to 62.57 days on average.

Days on market typically continue its decline until sometime in early May, when inventory increase accelerates and showings start to wane. That is the time of year when sellers want to sell, but buyers want to ride their bike or take more vacations.

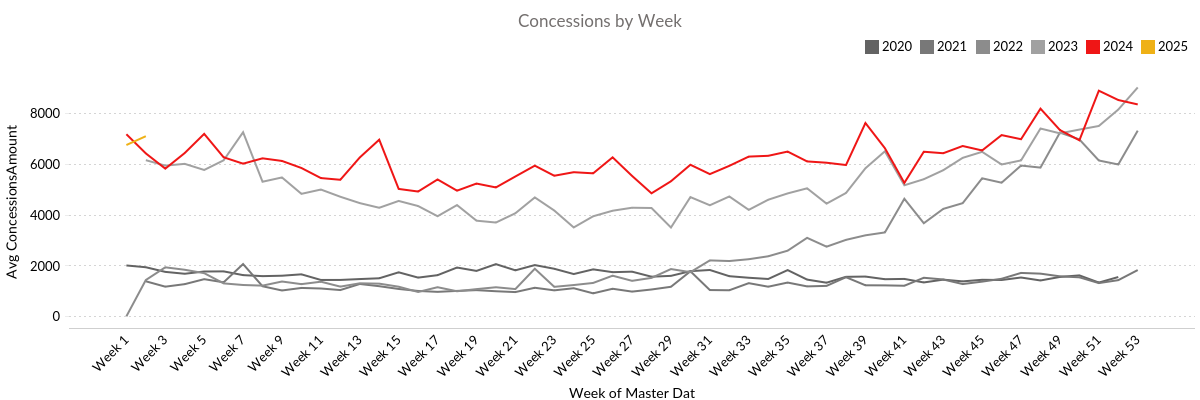

Seller Concessions

Maybe this is the new norm? With only slight variation, for decades seller concessions average about $1,500 per contract, but starting June of 2022 when interest rates accelerated their climb, seller concessions began to rise.

In 2024, seller concessions averaged closer to $6,000 per contract and we are starting out the year similar to last year ending last week at $7,083 per contract.

Seller concessions have simply become a standardized asset for buyers, used for property repairs, closing costs or rate buy-downs. If rates remain elevated, expect seller concessions to follow a similar pattern as last year.

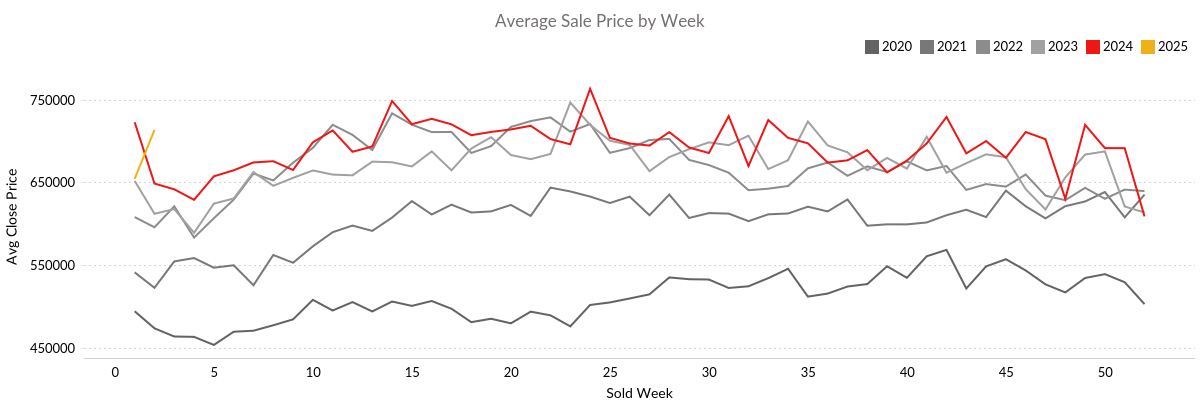

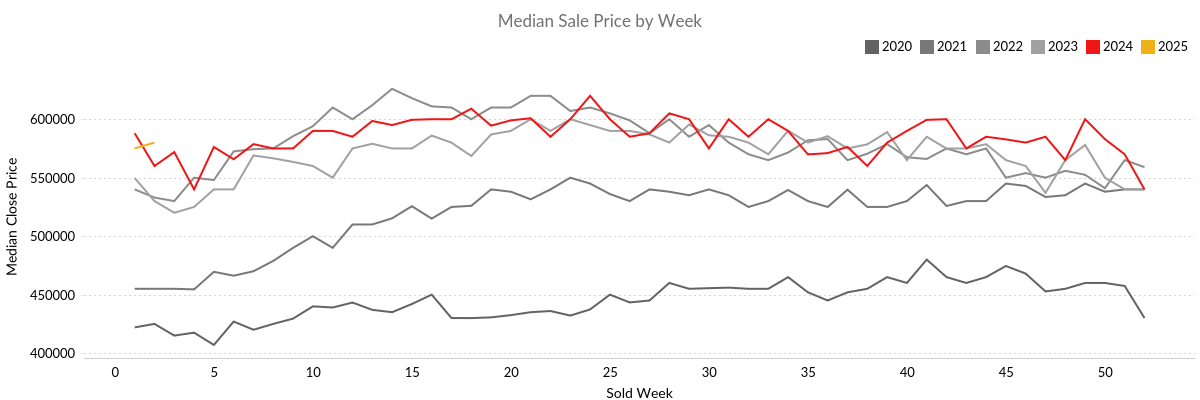

Price

It’s way too early in the year to see any trends in statistics. We can only predict aspects of this coming spring market because of historical patterns for things like inventory increase and days on market decline.

But price is the final outcome, the result of all other market factors poured into a big pot of real estate soup. And unless inventory crosses the 15,000 home mark and interest rates hit 8%, home values will remain steady to modestly increasing.

And make no mistake, short of some catastrophic geo-political event there is no scenario under which home values crash in Colorado. Why? Because a crash in values would require homeowners bailing out of their homes where foreclosure is more attractive than homeownership. And the market fundamentals simply do not exist for that.

Unlike 2008 where the average buyer was putting down less than 5% on their loan and had a credit score well below 700, today’s market is stabilized by the vast majority of homeowners having exceptional credit, lots of equity and payments on their current mortgage that are lower than the rent they would pay for the same or even lesser home. Sellers are not bailing out of their property.

So what is the prediction for price this year? Modestly appreciating. Last week saw a big jump in the average sales price to $713,000 or the highest we’ve ever seen this time of year. But, that is most likely an anomaly with one or two very expensive homes selling and throwing off the average.

However, the median home price is almost never up this time of year and sure enough last week saw a median home price increase from $575,000 to $580,000. This is surprising since these are closed sales that went under contract in mid-December, the slowest market in the last 12 years.

So what does this mean? Likely nothing. Let’s not hold our breath each week and hang our emotions on price movement. From current prices, home values will increase this spring, but let’s not get too excited about appreciation or any one data point just yet.

This market has a lot to prove out this year between interest rates, buyer decision making and inventory levels.