WEEKLY MARKET BRIEF │ NOVEMBER 19, 2024

In a post-election relief of “finally, it’s over”, buyers got back to business. While half the country may have been disappointed with the election outcomes, and interest rates are the highest they’ve been since the end of July, the pre-election “lul” of showings turned into a one week spike of buyer activity. We’ll see if that is sustained. We also experienced a modest increase of new listings hitting the market and properties going under contract.

But let’s not look at any of this activity as a silver lining to a bad market. We are in a very solid market with great fundamentals, with an interesting factor we haven’t seen in a while. Buyer behavior that doesn’t seem to be as sensitive to interest rates as they have been.

In the meantime, it’s important to know that history is repeating and the seasonal market changes are doing exactly what we expected. These are not bad signs. These are not things to be concerned about. These are seasonal market shifts we’ve been saying all buyers and sellers should be prepared for.

And in about 60 days, we will most likely see all of the below begin a radical shift into spring market conditions. But for the next 60 days:

- Days on market are spiking.

- Seller concessions are rising.

- Offers under asking are increasing.

- Price reductions are increasing.

- Showings will slow going into Thanksgiving week and through the rest of the year.

- Inventory will continue to decline as more homes are pulled off the market for the holidays, buyer activity remains seasonally steady and fewer listings hit the market.

- The average sold price will slide, before beginning to rise in early February.

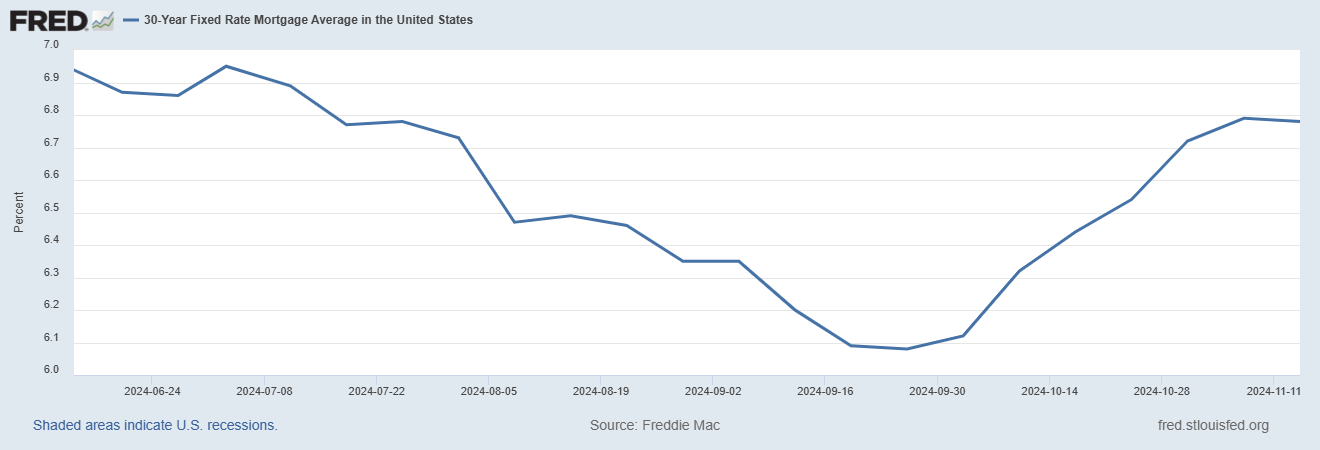

Interest Rates

Yes, rates spiked for the last 60 days. No, mortgage rates have almost nothing to do with what the Federal Reserve does or who is elected president, other than the emotional response to what these things potentially mean. Over the last 60 days, the Federal Reserve dropped the overnight funds rate by .75% and mortgage rates went higher by .75%. That’s because the lower Fed rate meant cheaper capital for business growth, which gives investors hope for strong returns in the equities market, and instead of buying bonds, they buy stocks. As money is pulled out of bonds, mortgage rates go higher.

While there are many other factors that point to signs of economic weakness such as the labor market, manufacturing, household debt and national debt, and interesting new policies from the incoming administration that will likely drive government jobs markedly lower through cost cutting, creating a short term spike of unemployment, believe it or not, these are good signs for interest rates. As investor confidence slides, investment in bonds increases, which decreases mortgage rates.

We’ll see how long the Trump investor euphoria lasts.

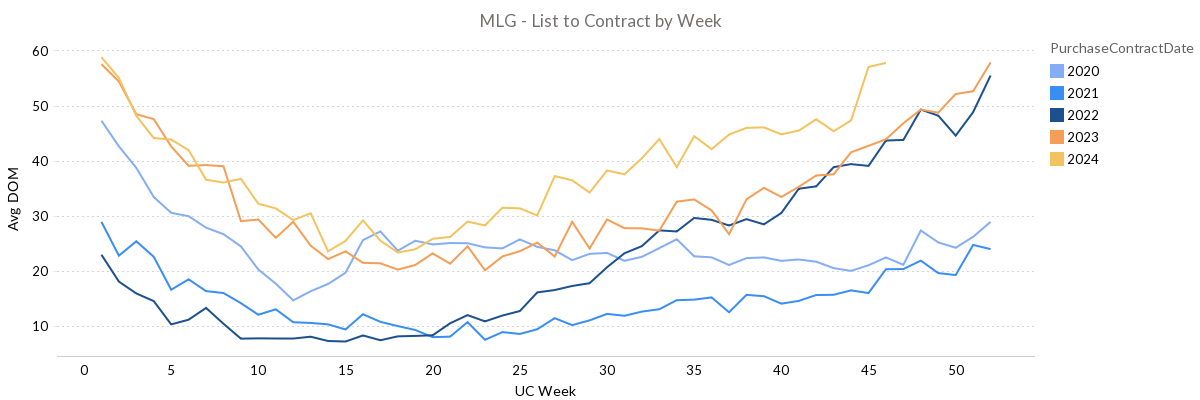

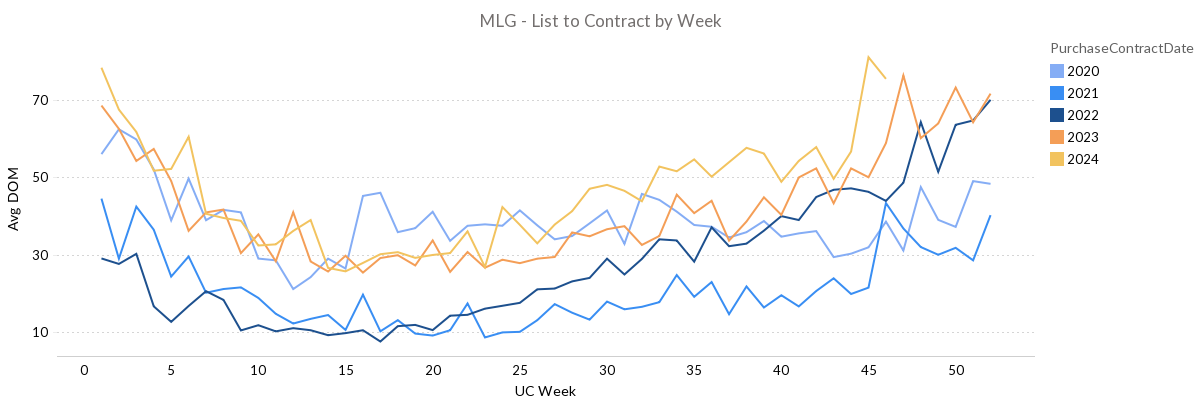

Days on Market

We’ve been saying that the market should expect average days marketing time of a property to surpass 60, maybe even 70 by year end. As you’ll see in the showings calculations later in this article, there is even an argument for DOM to hit over 90 this year. Well last week’s days on market were revised up after the MLS cleaned its data and we are now over 57 days on market, with 6 weeks to go before year end.

Last year ended with 57.84 days on market, today we sit at 57.42. Expect marketing time to get longer before year end, which means seller patience and buyer purchasing authority.

But sellers would do well to remember that days on market begin to drop rapidly after the first of the year. Buyer activity ramps up quickly after January 1, but seller activity doesn’t begin to really ramp up until the middle of March to early April. Sellers who are on the market early season will likely have less competition for the very active buyers.

For larger homes, the spike in days on market was even greater. For homes over 3,000 square feet, days on market hit an average of 80.93 days, compared to a high of 76.21 days last year. Why did the days on market trend down toward the end of the year last year? Likely because bigger homes are hosting families for holidays and they took their home off the market.

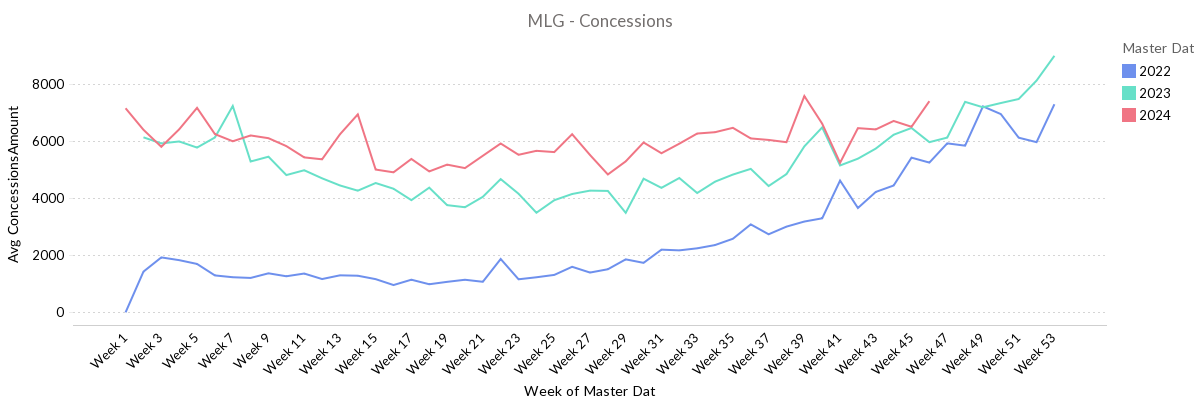

Seller Concessions

The upward trend toward year-end is happening, with the average contract ending last week with seller concessions of $7,409. With interest rates remaining elevated, expect concessions to end the year over $8,000 per contract.

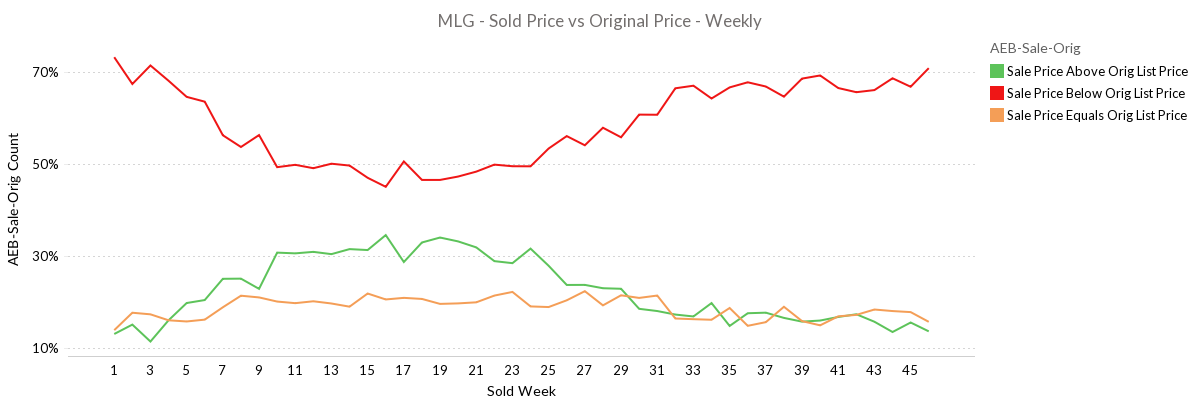

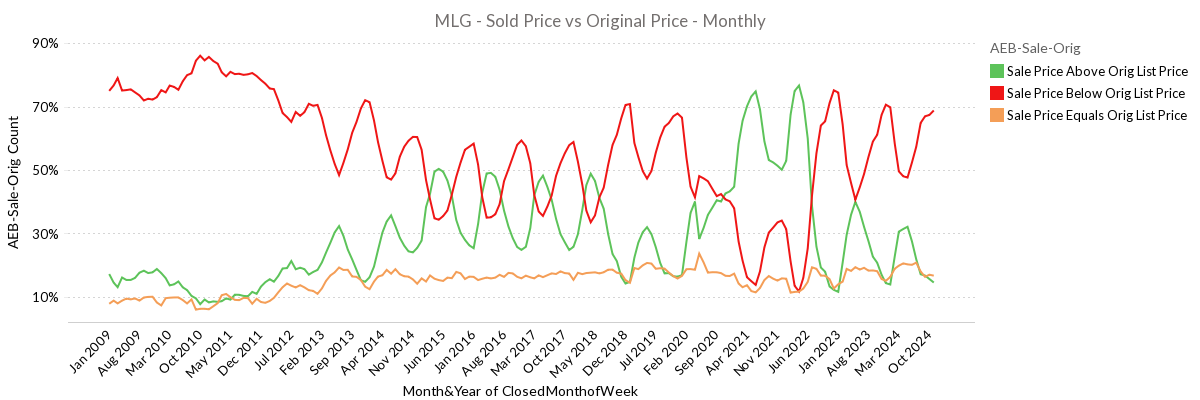

Offers Over/Under Asking

70.8% of properties sold under the original asking price last week. At this pace, expect that number to exceed 75%, maybe even 80% by year-end.

Note-the all time high for percentage of properties selling under the original asking price was in October of 2010, at 86%.

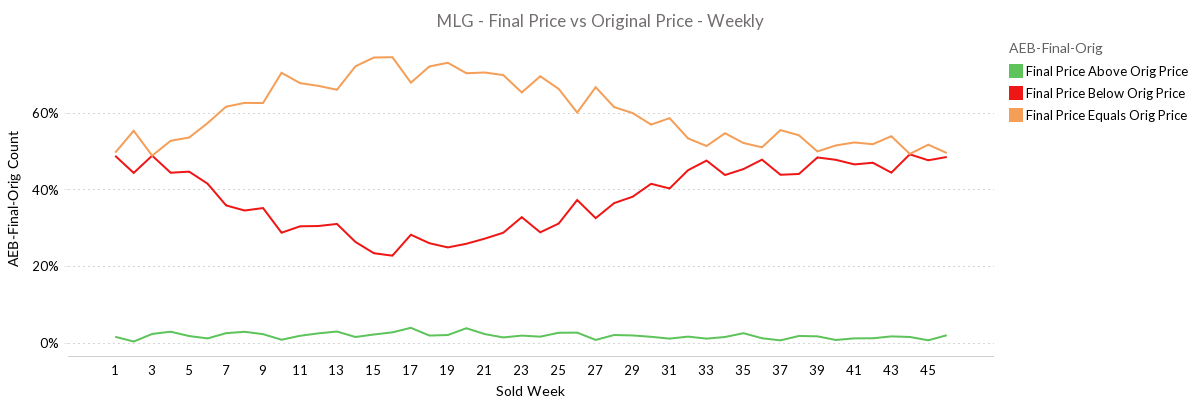

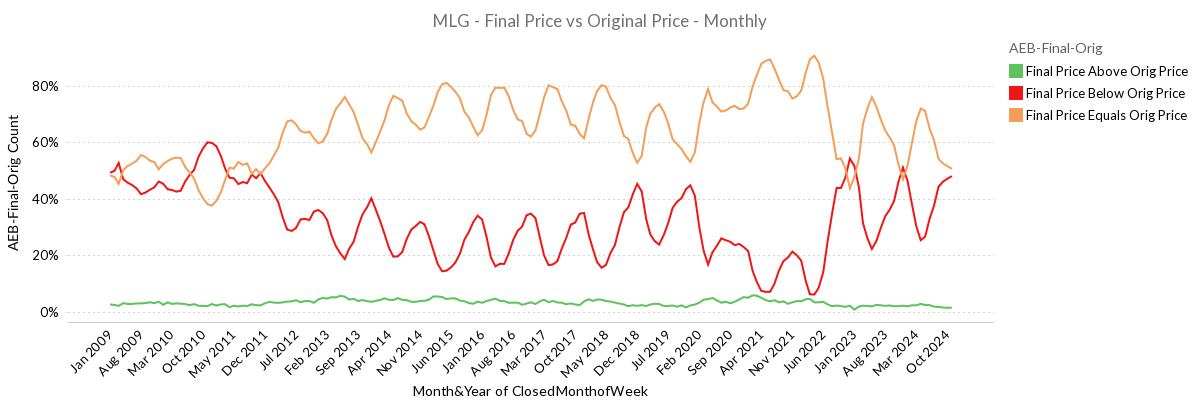

Price Reductions

Sellers aren’t ever stubborn, right? As of last week, 48.4% of all listings have experienced a price reduction. But that still leaves 49.5% who haven’t reduced price and oddly, 2.1% who have increased price.

But as we look at the history of price reductions, we’d be hard pressed to see the percentage of homes reducing price to get much greater than 53-55%. In history’s worst market, 2010, November and December price reductions topped out at 60%.

The 40% remaining was most likely hopeful sellers who were able to wait for the spring market. We’ll see much of the same this year.

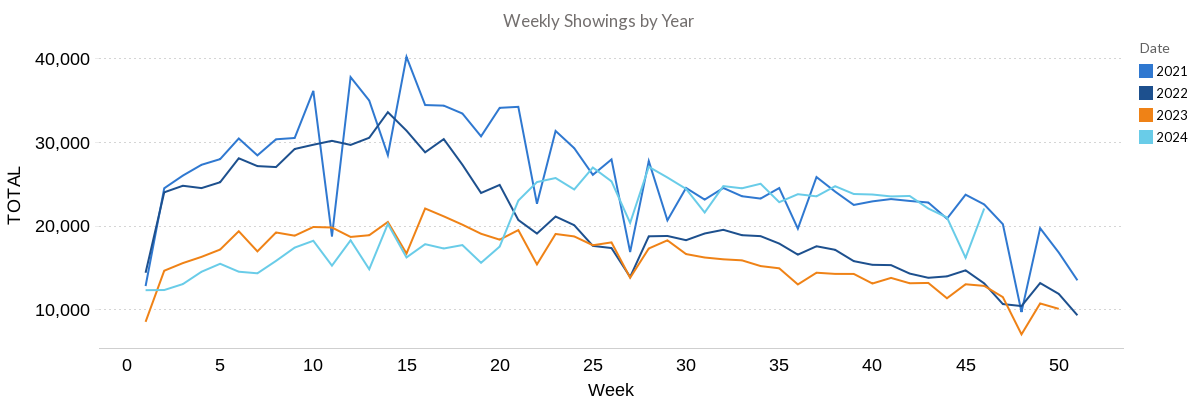

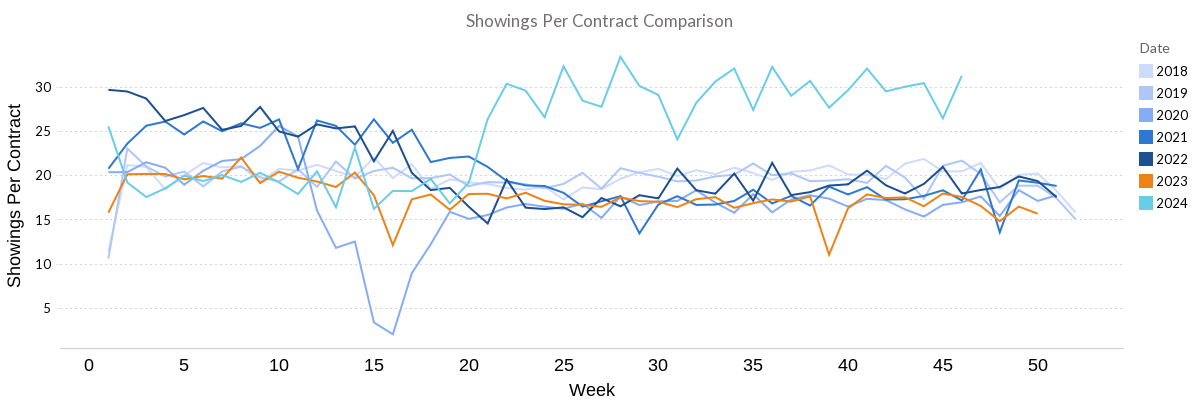

Showings

Showings jumped 39% last week to 22,046 on declining market inventory. Expect showings to cool off markedly through the holidays as they have historically. But these showings with high interest rates are demonstrating significant market demand which is a great lead indicator for a strong spring 2025.

However, buyers once again demonstrate an annoying amount of patience with the average property needing 31.27 showings before going under contract.

With showings per listing at only 2.17 last week, that means we are headed toward over 90 days on average marketing time. Sellers, hang on.

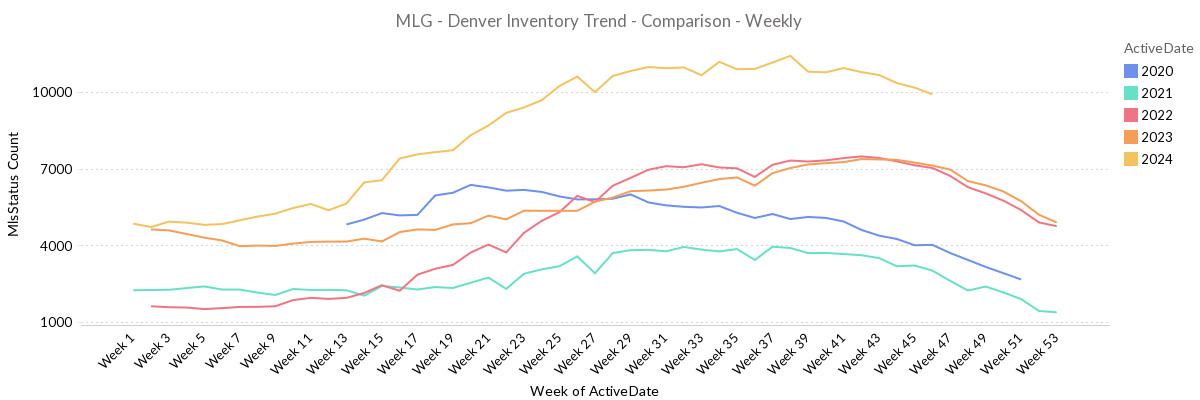

Inventory

Nothing remarkable happened last week. With more sellers taking their homes off the market, contract activity seasonally stable and fewer homes hitting the market this time of year, inventory is sliding into holidays home plate.

Last week ended with 9,902 homes available for sale. We’d estimate ending the year with about 7,500 homes on the market.

Conclusions

For the next 60 days sellers need to be prepared for:

- Longer marketing time

- Offers below asking

- Increasing requests for seller concessions

- Price reductions of competition

If sellers can be patient and wait for the early January turn (only 45 days from now), they’ll start to see these conditions lift.

Once again, buyers who can afford to buy right now may be able to negotiate incredibly favorable contract terms.