WEEKLY MARKET BRIEF | FEBRUARY 25, 2025

Seller concessions and days on market remain elevated, reflecting plentiful inventory and patient buyers. However, contract activity is now outpacing the past two years, illustrating a strong seasonal shift. Meanwhile, average sold prices continue to rise, more offers are coming in above asking price, and price reductions are on the decline.

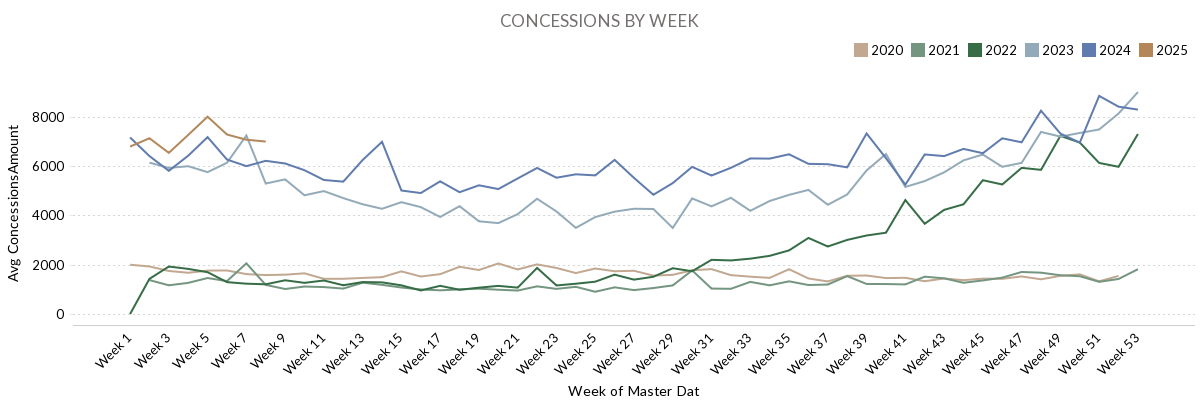

Seller Concessions

Seller concessions are the dollar amount contributed by the seller at closing for the buyer’s benefit. These can cover property repairs the seller opts not to complete before closing, rate buy-downs, and other closing costs tied to the buyer’s loan.

Historically, concessions have averaged between $1,500 and $2,000. However, after a two-year run-up in home prices followed by a spike in interest rates, concessions became standard in most contracts by 2022.

Today, concessions are averaging $6,995—the highest on record for this time of year—driven by elevated interest rates (though on a downward trend) and higher inventory, which shifts more negotiating power to buyers. We expect concessions to moderate over the next couple of months as increasing buyer activity strengthens sellers’ bargaining positions, but sellers should still anticipate some ask for concessions in most contracts.

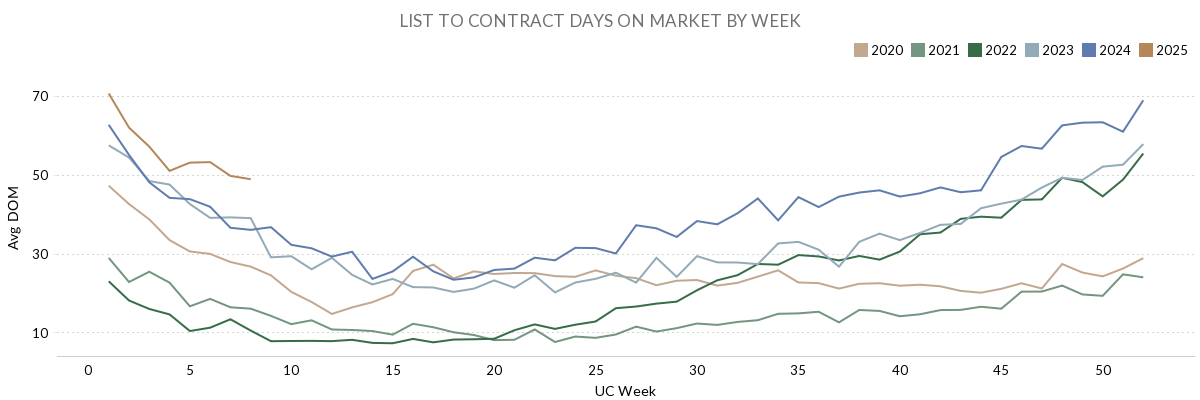

Days on Market

Typically, days on market plummets from early January through early April before climbing again toward year’s end. However, this year’s pattern has taken a puzzling turn: for the past five weeks, days on market has hovered between 49 and 51 days, defying the usual seasonal drop.

The explanation isn’t complicated: rising inventory, patient buyers, and elevated interest rates are slowing the market’s pace. For the first time since 2012, we aren’t seeing a rapid decline in days on market.

This is an early indicator worth watching. Should days on market remain elevated, buyers could gain considerable leverage this spring, potentially resulting in more price reductions and fewer offers over asking price. But we’re not there yet. Buyer activity remains solid, and even a small dip in interest rates could spur the market and swing the advantage back to sellers.

Contracts

Last week recorded the highest weekly contract count in the past three years, and only slightly below the frenzied pace of early 2022. We believe this affirms the trend we anticipated. There is significant pent-up demand from the last three years of suppressed market activity, suggesting that real estate may remain resilient in almost any interest rate, political, or economic environment.

We will see how this pattern takes shape over the coming weeks, but with a slight downward trend in interest rates, another spike in contract activity is likely.

Price Reductions

Currently, 41% of listed homes have undergone at least one price reduction, down from 57% in late December 2024. While it can be a wise strategy for sellers to push for maximum equity, they should stay flexible and be prepared to adjust prices based on market feedback—especially given today’s unpredictable interest rate environment and higher inventory levels.

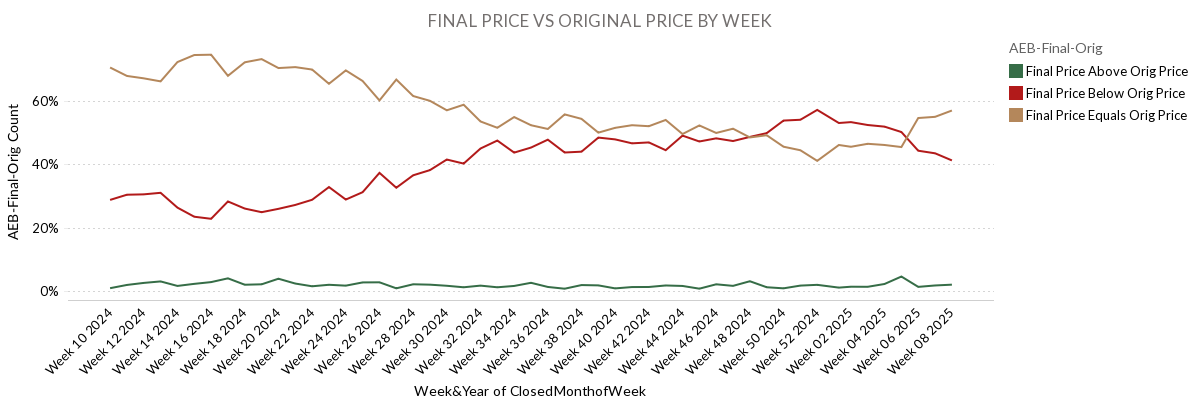

Offers

Offers above the asking price are trending as anticipated, with 22.4% of properties last week closing over their original list price. Keep in mind, these numbers reflect homes that went under contract about 30–40 days ago.

40 days ago, interest rates were more than 10% higher than they are today. While elevated inventory and longer days on market could lead to more price reductions, declining interest rates and robust buyer activity still point to a seller’s advantage as we head into the 2025 spring market.

40 days ago, interest rates were over 10% higher than they are today and while elevated inventory and longer days on market suggest the potential for more price reductions, declining interest rates and strong buyer activity suggest sellers are still in the drivers seat for the 2025 spring real estate market.

Conclusion

The market is showing signs of both resilience and caution. Elevated concessions and days on market hint at buyer-friendly conditions, yet climbing contract activity, fewer price reductions, and a rising share of offers above asking illustrate a strong spring season for sellers. Amid shifting interest rates, buyers and sellers alike should remain flexible—staying mindful of market feedback and prepared to pivot as conditions evolve.