WEEKLY MARKET BRIEF | JANUARY 28, 2025

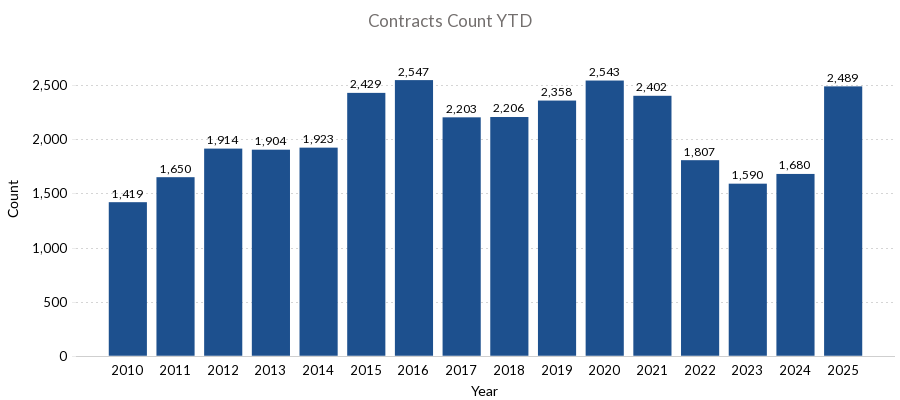

Inventory sits 47% higher than at this time last year, while days on market has dropped by 36% since January 1. Year-to-date home showings are only slightly below the two busiest years in Colorado (and U.S.) real estate history—2021 and 2022. This strong showing activity is already translating into more contracts, making 2025 year-to-date the third highest in the last 15 years.

Current Market Conditions

- At present, 53% of properties are experiencing a price reduction, up from about 45% this time last year. While we expect fewer price reductions in the coming weeks, it’s wise to temper expectations. Higher inventory and interest rates continue to give buyers a competitive edge—though we anticipate this market dynamic will shift in the coming weeks.

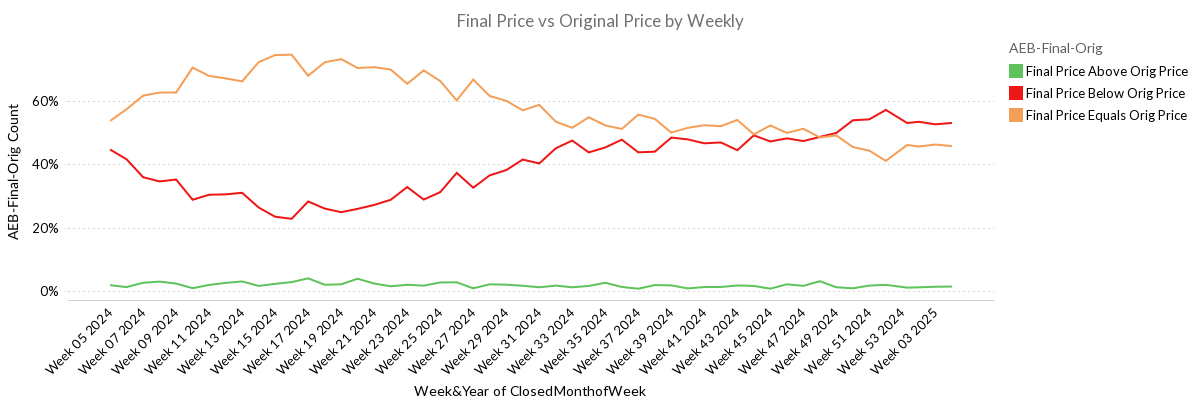

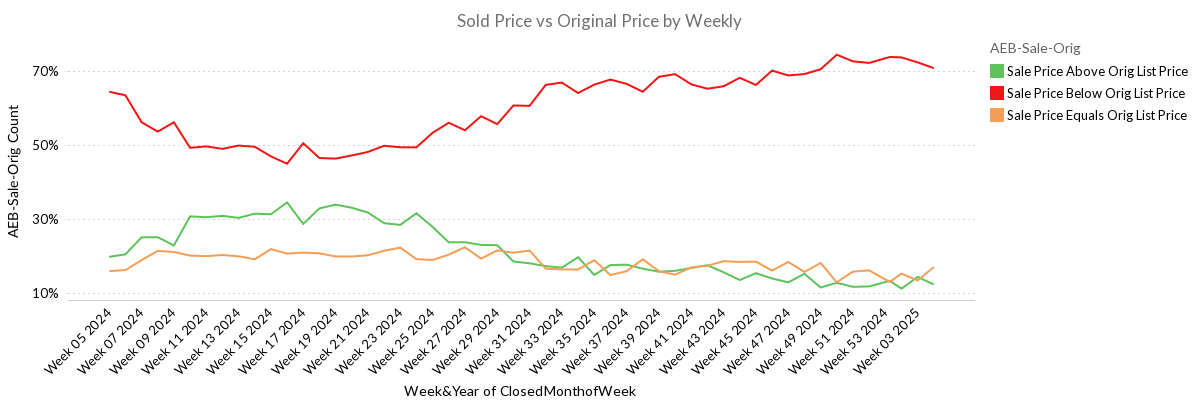

- Currently, 71% of properties are selling below their original asking price, compared to 65% at this time last year. Remember, this is a “lag measurement” based on contracts signed 25–40 days ago, so we can expect this figure to shift as the market heats up.

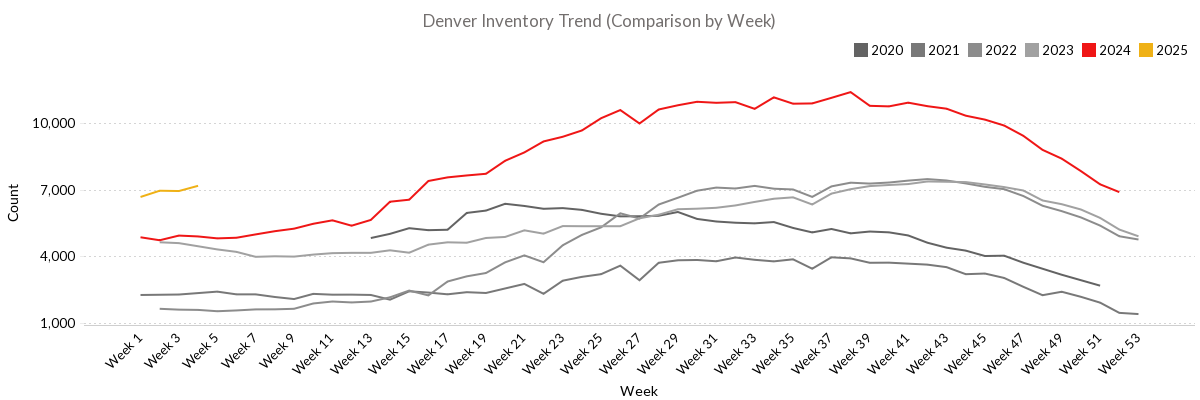

- Inventory climbed slightly this week, with 1,006 new listings—only 7% below the busiest year in Colorado real estate history (2021). We ended the week with 7,179 homes for sale, up from 4,892 one year ago.

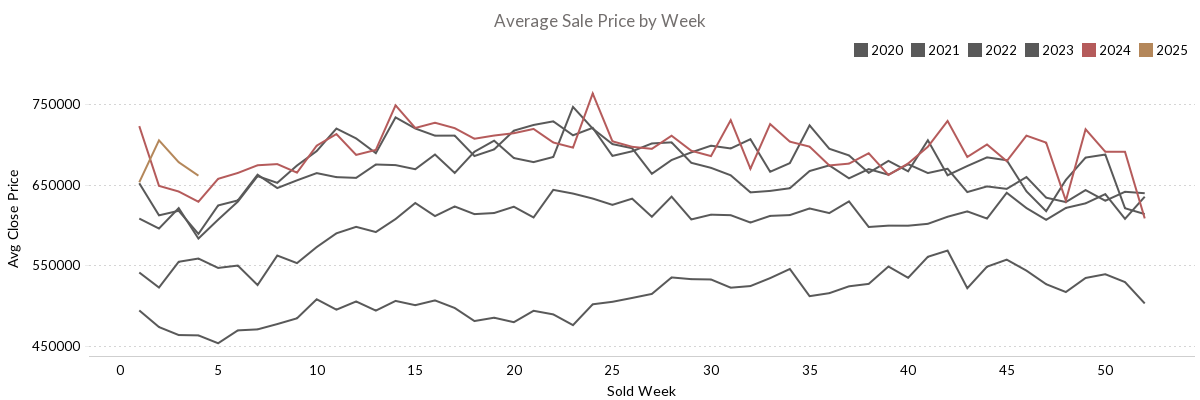

- Prices dipped for the second week in a row, ending last week at an average sold price of $661,096. This is typical for early in the year, as price data also lags, reflecting properties that went under contract in late December. Expect sold prices to start rising next week and continue through early May, before following their usual gradual decline.

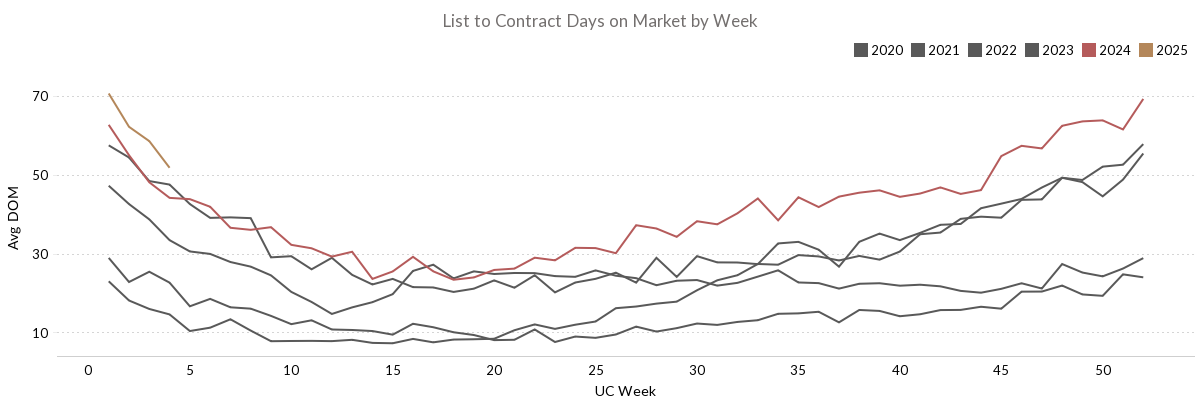

- Days on market reached a 13-year high of 71 days in early January but has since dropped to 52 days. The decline is partly due to some listings being removed, increased buyer activity, and new listings pulling the average down. However, if inventory remains elevated and interest rates stay higher, days on market likely won’t dip below 30 compared to a low of 23 days last year.

Many variables are at play in our economy, financial markets, and government policies. Markets appear enthusiastic about the new administration, and buyer activity remains incredibly strong. Although the outlook is hopeful, the true economic impact is still unclear—especially when it comes to interest rates.

Interest rates will drive buyer decisiveness. A 30-year fixed mortgage rate has risen by a full percentage point in the last 120 days, causing buyers to take more time and demand more favorable terms. We anticipate a traditional spring market where sellers regain some leverage from mid-February through late April, but unless rates drop, buyers will remain cautious. Affordability concerns will continue to temper market velocity.